Internal First, Portfolio Second

The sequencing mistake most PE firms make with AI programs. And the 90-day internal win that changes the calculus.

Blake Aber · Predicate Ventures · 2026

The pattern I keep watching: a PE firm announces an AI initiative for its portfolio companies. The announcement is LP-facing. The initiative is visible. The firm looks like it's ahead of the curve.

Eighteen months later, the portfolio companies are still running pilots. The AI initiative is still being announced. The GP team has spent considerable time running workshops and writing frameworks. Portco results have been uneven.

The problem isn't that the firm was wrong about AI. It's that the sequence was wrong.

Why firms start with portfolio AI

The LP optics pull strongly toward portco visibility. AI transformation at the portfolio level is a thing you can describe in a fund letter. It sounds like value creation. It's what other GPs are talking about at conferences.

Internal AI (AI that makes the GP team's work better) is invisible from the outside. No LP ever asked a GP: "How much faster are you doing due diligence now that you've automated memo synthesis?" The incentive to publicize what's visible outweighs the incentive to build what's useful.

So firms start with portfolio AI. The GP team hires a "Head of AI" or brings in consultants. The portcos get workshops. Some pilots run. Some don't.

The problem with portfolio AI first

Here's what the firms that sequence this way discover at around year two: they're trying to provide AI support to portfolio companies without having built the AI muscle internally.

When a portco CTO calls to ask for advice on eval harness design, the GP team doesn't have a practiced answer. They haven't built an eval harness themselves, so they can't speak to why production AI is mostly harness and only a little model. When a portco initiative stalls at the organizational seam between product and engineering, the operating partner doesn't know how to diagnose it. They haven't worked that seam internally.

The advice is conceptually correct but operationally thin. The portco can tell. The relationship suffers.

Firms that skip internal AI first are usually still doing portfolio AI three years later with thin results. They haven't compounded, because you can't compound from a base you don't actually have.

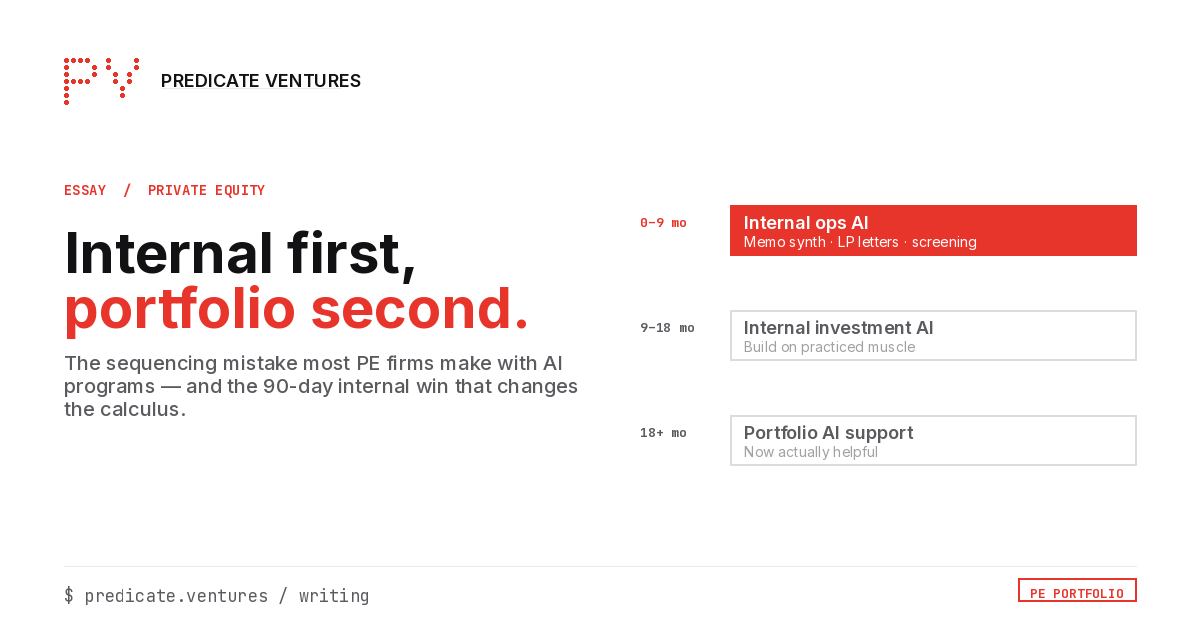

The sequence that works

Internal ops AI first (0-9 months): Start with the GP team's own workflows. Three of them work in 90 days or less, without enterprise-scale infrastructure:

- Due diligence memo synthesis. A named analyst spends 8-12 hours per deal synthesizing interview notes, financials, and reference calls into a memo. AI reduces this to a 90-minute review and editing job. Ships in 30 days. Immediate compounding.

- LP reporting automation. The quarterly LP letter has a predictable structure and a predictable set of inputs. AI drafts 80% of it. The senior team reviews and personalizes the 20% that matters. Ships in 45 days.

- Deal-screening signal surfacing. The analyst team is reading a thousand news items and LinkedIn posts a week looking for signals that match the investment thesis. AI surfaces and scores the relevant ones. Human judgment remains the gate. Ships in 60 days.

Internal investment AI (9-18 months): Build on the internal muscle. Now the GP team can talk about AI from experience, not from frameworks.

Portfolio AI support (18+ months): Now you're actually helpful to portcos. You've solved the problems they're facing. You can speak to the organizational seam question, the eval harness question, and the build-versus-shepherd staffing question that sinks junior-IC-led programs from lived experience.

The question worth asking

What is the internal AI your GP team runs on today?

Not what you've recommended to portcos. Not what you've told LPs. What is the AI that your analysts and partners actually use, every week, to do their jobs faster and better?

If the answer is vague, that's where the AI program actually starts.